“What has changed a lot in the BHP iron ore business is their costs, production costs have been driven down to 17 Dollars per ton, an astonishing figure. To think that it didn’t matter when the elevated iron ore price meant that cost cutting initiatives were something to happen later. Cost cutting had a massive positive impact of 3.8 billion Dollars, a negative impact of 15.2 billion Dollars as a result of much lower commodity prices. That is the biggest problem, this is possibly the finest in quality of all the mining companies, yet, like everyone else, they cannot control the prices.”

To market to market to buy a fat pig. Whoa, more dumbness. A panic close on Wall Street last evening. Stocks reversed a nearly three percent gain through the day to end over a percent down, touching the lowest closing levels for the year. It was really a sign that the jitters in equity markets never go away. I do not like to look at charts of equity markets and predict what is going to happen, that is even sillier. Drawing lines on a graph and suggesting x or y happens next is about as useful as predicting the weather in December based on today. Or (cheeky here) whether Chelsea FC are going to break into the top 10 of the BPL. Kidding, of course they are. We will get back to the markets in New York in a second, first it is time for Jozi, Jozi. Locally our markets roared yesterday, reports of the death of the global economy were greatly exaggerated. That was of course paraphrasing Mark Twain, where in fact his cousin was ill.

Expect to give up all those gains from yesterday in the early part of the trade. In the same breath as me saying I do not like charts, let me try and explain why this sell off feels so very bad, by using a uhhh ummmm, a chart. For most of this year the biggest market in the world, the S&P 500 has been stuck in a very narrow band. Very narrow in fact. I have circled in red (thanks CNNMoney for the graph) the period of great stability until just over two weeks ago.

Note the serious sell off in the last two weeks. By drawing any sort of line on that graph to the right is just as good as guessing. There is a story of Buffett being handed a graph and asked his opinion, he purportedly asked which way around he should hold the paper. I am not too sure about whether that is too true, it is however funny. Technical analysis is not for me, it is classic pattern recognition. I was on TV, Monday lunch time and was asked about the similarities between 1987 and now, there are similarities emerging said Lindsay Williams from CNBC Africa. I said to him, when I encounter people talking about two different periods in history I always answer with a facetious question, “how many iPhones did they sell back then?” The answer is obviously none.

I was rapped over the knuckles by Lindsay when he said I could not use the Benjamin Graham example of choosing your stocks like groceries and not perfume, he said to me that they sold no iPhones back then. We ran out of time when I tried to stick the boot back in I failed, we had run out of time. Darn, live TV.

I made a similar quip yesterday on live radio, using the legendary investor Peter Lynch’s line: “I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.” I lost many points with Michael for bringing this up over and over again. He hates me for it. Anyhow, that statement became very evident yesterday when the local GDP number was released for the second quarter (we are nearly finished month two of the third quarter) and we were met by a contraction, in Rands too, down over a percent when measured against the first quarter of this year and then the figure is annualised. Perhaps the economy has improved a little between now and then. There was NO reaction from the equities markets, none whatsoever from the currency. Perhaps it was “priced in” or more likely equity markets and currencies are driven by the global flows.

Remember and recall each and every time there is an economic release, the stock market is not the economy and the economy is not the stock market. That is possibly what Peter Lynch meant, spend your time focusing on the companies and their prospects, their price relative to those same said prospects, rather than the economy.

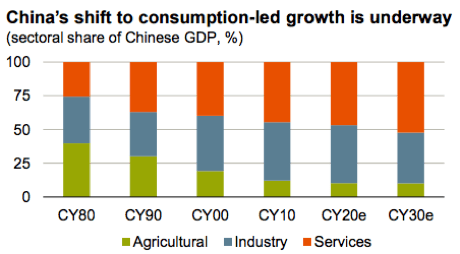

Whilst the Chinese have cut rates for the fifth time since November (another cut after their market had closed yesterday, about midday locally) in order to shore up their economy, you should not worry about the health of that economy. BHP Billiton in their results yesterday had something interesting to say about the Chinese economy, the shift to consumption:

“In line with our expectations, the economy is growing more slowly, though off a higher base, as it matures over the medium term and the government’s reform program promotes domestic consumption over investment. We expect near-term volatility to continue as the authorities press ahead with reform in a cautious but sustained manner as they seek to improve the efficiency of capital allocation in the economy while maintaining support for employment. However, our robust longer-term outlook for China remains intact as the economy transitions.”

There is an associated graph of their expectations of the makeup of the Chinese economy, a slide that explains how the shift is unfolding over the next decade and a half. Of course this is just guessing, a very good guess, this was not just thumb sucked:

The most important “thing” to come out of the BHP Billiton results yesterday was their downgrading of peak Chinese steel production. Which is very important for their iron ore and metallurgical coal business. Of course this is very important for all iron ore producers globally. BHP reckons that, from their presentation: “we expect China’s crude steel production to peak between 935-985 Mt in the mid 2020s”. The previous guidance was at the high point 1100 Mt.

What has changed a lot in the BHP iron ore business is their costs, production costs have been driven down to 17 Dollars per ton, an astonishing figure. To think that it didn’t matter when the elevated iron ore price meant that cost cutting initiatives were something to happen later. Cost cutting had a massive positive impact of 3.8 billion Dollars, a negative impact of 15.2 billion Dollars as a result of much lower commodity prices. That is the biggest problem, this is possibly the finest in quality of all the mining companies, yet, like everyone else, they cannot control the prices. And whilst the quality will remain, the focus will be on long term shareholder returns, the market remains oversupplied in some very key commodities. Oil and iron ore. The demand side looks lukewarm, another big infrastructural program from perhaps India needs to emerge for prices to get a serious lift.

The dividend was increased marginally, earnings were crushed as revenues fell nearly one quarter. We continue to lighten our commodity exposure across the board and have been doing so for some time now. No matter how good the management team, no matter how good the cost control, the price is controlled by the market. Which is not really fair, the price for all products is essentially set by the market. However, as we know, a longer dated bet on higher commodity consumption (which is expected as we continue to urbanise) is somewhat a bet against human innovation.

As production costs decrease as a result of innovation, the marginal miners will be flushed, it will be ugly and in the end the quality majors will prevail, BHP will still be top of the pile. The cycle may be very deep from peak to trough, and as people who were in commodity markets for thirty years will tell you, for the first twenty years basically nothing happened. I shall leave you with a 30 year graph from IndexMundi of the Iron Ore price, for you to see what I mean. Literally nothing happened for 20 years.

That is right, I recall a headline that I once posted which said something along the lines (when referring to rent resources tax globally on commodity companies being mooted by “smart” governments) “You did not make that iron ore price”. Exactly, the market made the price.

Linkfest, lap it up

Perspective matters and so does knowing what your timeframes are – The Great Divide – Traders versus Investors. The biggest point I got out of the post was that GDP is probably underestimated using current methods. We also need to focus on stock gains over the last few years in connection with the underlying strength of the global economy.

Charlie Munger is one of the best investors out there and one of the smartest people around – 10 Underrated Charlie Munger Quotes

Things do change, maybe not at the speed that people want them to though – The evolution of American energy consumption since 1776. If we get most of our energy out of renewable sources in the next 100 years, it is essentially our globe doing a total ‘180’ in a lifetime. Which is nothing in the grand scheme of things.

Imagine the possibilities from having a selected gene pass through generations. This has the potential to wipe out diseases that are transferred from parents to children – The most selfish genes

Home again, home again, jiggety-jog. Stocks are likely to be lower again today. Chinese shares are a little higher after a volatile session. Stay the course and buy the quality, the message from yesterday is clear, if you can get the same quality asset at a lower price, what is not to like about that? There are always long dated time frames, if however you are saving for retirement, you will want lower share prices in perpetuity, to lock in lower entry prices along the way. If you are older and reliant on the gains in the short prices to supplement your income, this is an unwelcome and nasty fall in your NAV, it leaves you reaching for the antacid. Worry not, the storm passes. The shouting voices and the chasing your tail strategy during a time like this proves to have once again been the wrong one. As in Braveheart when the horses are charging at you, you should hold ….. hold ……. hold!

Sent to you by the Vestacters, Sasha, Michael, Byron and Paul.

Follow Sasha, Byron and Michael on Twitter

087 985 0939